Developing bad financial habits can have a significant impact on your financial stability and security. Many individuals struggle with managing their finances effectively due to certain behaviors that negatively affect their financial health.

Understanding and changing these detrimental financial habits is crucial for achieving financial freedom. By identifying and breaking these habits, you can take control of your financial situation and make progress towards your financial goals.

Key Takeaways

- Recognizing bad financial habits is the first step towards financial stability.

- Changing detrimental financial behaviors can significantly improve your financial health.

- Adopting good financial habits can lead to achieving financial freedom.

- Understanding the impact of financial habits on your financial situation is crucial.

- Breaking bad financial habits requires commitment and discipline.

The Hidden Impact of Daily Financial Decisions

Daily financial choices, though seemingly insignificant, can collectively lead to substantial financial consequences over time. These decisions, often made without much thought, can have a profound impact on our financial health.

How Small Choices Compound Over Time

Small financial decisions, such as buying coffee every morning or subscribing to multiple streaming services, can add up over time. For instance, spending $5 daily on coffee translates to $150 monthly. Cutting back on such expenses can lead to significant savings.

The Psychology Behind Self-Sabotaging Money Behaviors

Understanding the psychology behind our financial decisions is crucial. Emotional spending, often triggered by stress or boredom, can lead to self-sabotaging financial behaviors. Recognizing these patterns is the first step towards changing them.

Here are some common self-sabotaging financial behaviors:

- Impulse buying

- Not budgeting

- Ignoring savings

By understanding how our daily choices impact our finances and recognizing the psychological triggers behind our spending habits, we can take steps towards better financial management.

Impulse Spending: The Silent Budget Killer

Emotional triggers and clever marketing tactics often result in impulse spending, a major obstacle to effective money management. This behavior can lead to significant financial strain over time, as unplanned purchases accumulate and budget stability is compromised.

Emotional Triggers Behind Unplanned Purchases

Impulse buying is often driven by emotional states such as stress, boredom, or the desire for instant gratification. Recognizing these emotional triggers is the first step towards managing impulse spending. By being aware of our emotional responses, we can develop strategies to mitigate their impact on our financial decisions.

How Marketing Tactics Exploit Financial Vulnerabilities

Marketing strategies are designed to exploit consumer vulnerabilities, often using tactics like limited-time offers, attractive discounts, or persuasive advertising to encourage impulse buying. Being aware of these tactics can help consumers make more informed purchasing decisions. For instance, understanding that “limited-time offers” are often marketing gimmicks can reduce the pressure to make unplanned purchases.

“The key to managing impulse spending is not just about resisting temptation but understanding the underlying motivations and external influences that drive such behavior.”

Practical Methods to Resist Spending Temptations

Several strategies can help resist the temptation of impulse spending. These include:

- Creating a budget and tracking expenses to monitor financial health.

- Implementing a waiting period before making non-essential purchases.

- Avoiding shopping when in an emotional state or under pressure.

Additionally, understanding the psychological aspects of spending can empower individuals to make better financial decisions. For example, studies have shown that consumers are more likely to make impulse purchases when they are in a positive emotional state or when shopping with credit cards, as it detaches the purchase from the actual money.

Living Paycheck to Paycheck Without a Safety Net

The anxiety of not having enough money to cover unexpected expenses is a common experience for those living paycheck to paycheck. This financial stress can be debilitating, affecting not just financial stability but overall well-being. Without a safety net, individuals are left vulnerable to financial shocks, making everyday life a challenge.

The Anxiety Cycle of Financial Instability

Financial instability can create a cycle of anxiety that’s hard to break. The constant worry about making ends meet can lead to stress, which in turn can affect job performance and overall health. This cycle can be self-perpetuating, making it difficult for individuals to get ahead financially.

Breaking this cycle requires a multifaceted approach, including effective budgeting and financial planning. By understanding where their money is going, individuals can identify areas to cut back and allocate funds more efficiently.

Creating Breathing Room in Your Monthly Budget

One of the first steps in creating financial stability is to assess and adjust your budget. This involves tracking expenses, categorizing spending, and making adjustments to free up more money in your budget. Practical budgeting strategies can help create breathing room, allowing individuals to save for emergencies and work towards long-term financial goals.

By prioritizing needs over wants and implementing a budget that accounts for savings, individuals can start to build a financial safety net. This not only reduces financial stress but also provides peace of mind, knowing that there’s a cushion against unexpected expenses.

What Are Some Habits That Are Ruining Us Financially?

Our daily habits can significantly impact our financial health, often in ways we’re not fully aware of. The way we spend, save, and invest on a daily basis can either strengthen or weaken our financial stability. Understanding these habits is crucial to making informed decisions that promote financial well-being.

Common Daily Behaviors Draining Your Wallet

Several daily behaviors can negatively impact our finances. These include:

- Mindless snacking or dining out, which can lead to unnecessary food expenses.

- Impulse buying, often triggered by attractive sales or marketing tactics.

- Not keeping track of small expenses, which can add up over time.

Being aware of these behaviors is the first step to changing them. By adopting more mindful spending habits, individuals can significantly reduce unnecessary expenses.

Social Media and the Pressure to “Keep Up”

Social media platforms often create pressure to “keep up” with the latest trends, lifestyles, or possessions. This can lead to overspending as individuals try to maintain a certain image or status. The constant exposure to advertisements and the highlight reels of others’ lives can foster a sense of financial inadequacy or competition.

To mitigate this, it’s essential to:

- Limit social media exposure or curate your feed to reduce financial stress triggers.

- Practice gratitude for what you already have, rather than focusing on what you perceive as lacking.

- Set clear financial goals that are not influenced by social media pressures.

The Subscription Trap: Digital-Age Budget Drains

With the proliferation of digital platforms, it’s easy to get caught in the subscription trap without even realizing it. Subscription services have become an integral part of modern life, offering convenience and access to a wide range of content and services.

However, the cumulative effect of these services can have a significant impact on your financial health. Many individuals subscribe to services they use infrequently or have forgotten about altogether, leading to unnecessary expenses.

The “Small Monthly Fee” That Adds Up Fast

Services like streaming platforms, software subscriptions, and membership programs often come with a “small monthly fee.” While $10 or $20 per month may seem insignificant, these costs can quickly add up. For instance, having multiple streaming services can cost over $50 per month, a cost that can be reduced by consolidating or canceling subscriptions.

Forgotten Subscriptions and Automatic Renewals

One of the most insidious aspects of subscription services is their tendency to automatically renew. Many people forget about their subscriptions, only to be surprised by the continued deductions from their bank accounts. Keeping track of these subscriptions is crucial to avoiding unnecessary expenses.

Auditing and Optimizing Your Digital Expenses

To avoid the subscription trap, it’s essential to regularly audit your digital expenses. Here are some steps to follow:

- List all your subscription services.

- Evaluate the usage and value of each service.

- Cancel any subscriptions that are no longer needed or used.

- Consider consolidating services to reduce overall costs.

By taking control of your subscription services, you can significantly improve your financial management and reduce unnecessary expenses.

Credit Card Mismanagement and Debt Accumulation

The convenience of credit cards can quickly turn into a financial burden if not managed properly. Credit card mismanagement is a widespread issue that leads to debt accumulation, affecting financial stability and overall well-being.

The Deceptive Comfort of Minimum Payments

Making only the minimum payment on credit card bills might seem like an easy way out, but it’s a deceptive comfort that can lead to a longer payoff period and more interest paid over time. This practice can trap individuals in a cycle of debt that’s hard to escape.

Interest Rates: The Hidden Cost Multiplier

Credit card interest rates can significantly increase the total cost of purchases. Understanding how interest rates work and how they can multiply the cost of debt is crucial for effective debt management. High-interest rates can turn a manageable debt into an unmanageable one if not addressed promptly.

Strategic Approaches to Eliminating Credit Card Debt

Eliminating credit card debt requires a strategic approach. This can include consolidating debt into lower-interest loans or credit cards, making more than the minimum payment, and using budgeting techniques to prevent further debt accumulation. Financial planning plays a key role in this process, helping individuals prioritize their debts and create a plan to become debt-free.

By understanding the pitfalls of credit card mismanagement and adopting strategic approaches to debt elimination, individuals can take control of their financial health and work towards a debt-free future.

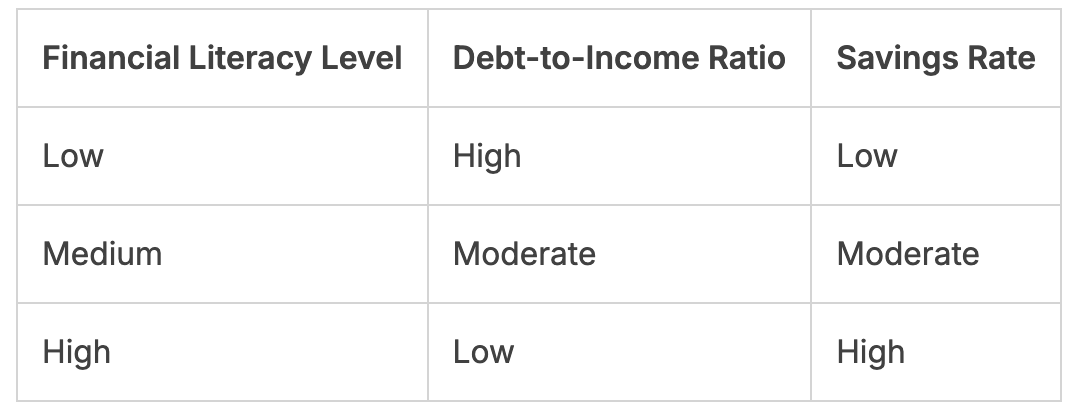

Neglecting Financial Education and Planning

Understanding personal finance is crucial, yet often overlooked, leading to financial difficulties. Financial education is not typically a part of the standard school curriculum, leaving many individuals to navigate complex financial decisions without a solid foundation.

The Cost of Financial Illiteracy in America

Financial illiteracy comes at a significant cost to individuals and the economy. A study by the Financial Industry Regulatory Authority (FINRA) found that nearly 40% of Americans lack basic financial literacy, leading to poor financial decisions.

The consequences include higher debt levels, lower savings rates, and increased vulnerability to financial scams. For instance, a survey by the National Endowment for Financial Education revealed that financially unsophisticated individuals are more likely to fall prey to investment fraud.

Resources for Building Your Financial Knowledge Base

Fortunately, there are numerous resources available to improve financial literacy. Online platforms like Investopedia and The Balance offer comprehensive guides on various financial topics.

“Financial education is a critical component of financial stability and security. By understanding basic financial concepts, individuals can make informed decisions that improve their financial well-being.”

National Foundation for Credit Counseling

Additionally, local community centers and libraries often host financial literacy workshops. Utilizing these resources can empower individuals to take control of their financial futures.

- Online courses and webinars

- Financial planning apps

- Workshops and seminars

Ignoring Retirement Planning in Your Prime Years

Many individuals overlook the importance of retirement planning during their peak earning years, a decision that can have long-term financial implications. It’s during these prime years that one has the greatest financial capacity to save and invest for the future.

The Mathematics of Delayed Retirement Savings

The power of compound interest is a critical factor in retirement savings. When you delay saving, you not only miss out on potential returns but also reduce the overall amount you can accumulate by retirement age. For instance, starting to save $500 monthly at age 25 yields a significantly larger nest egg by age 65 than starting at 35, due to the additional decade of compound interest.

Delaying retirement savings can result in:

- Reduced total savings due to fewer years of accumulation.

- Lower overall returns because of missed investment opportunities.

- Increased financial stress in later years if retirement is not adequately funded.

Simple Steps to Start Investing at Any Age

It’s never too late to start investing for retirement. Simple steps include setting up automatic transfers from your checking account to your investment or retirement accounts, taking advantage of employer-matched retirement plans like 401(k), and exploring low-cost investment options such as index funds.

Starting small and being consistent are key. Even modest, regular investments can add up over time, thanks to the power of compounding. For those who are behind, catch-up contributions to retirement accounts can be a valuable strategy.

Conclusion: Breaking Destructive Financial Patterns

Recognizing the habits that are ruining your finances is the first step towards achieving financial stability. Throughout this article, we’ve explored various daily behaviors and financial decisions that can have a significant impact on your financial well-being, from impulse spending and living paycheck to paycheck, to neglecting financial education and retirement planning.

Effective financial management is crucial for securing a stable financial future. By understanding the psychology behind self-sabotaging money behaviors and learning how to resist spending temptations, you can begin to adopt healthier financial habits. This includes managing your financial habits, such as auditing digital expenses, eliminating credit card debt, and starting to invest in your retirement.

By taking control of your money management, you can break the cycle of financial instability and build a more secure financial future. It’s essential to stay committed to your financial goals and continually educate yourself on best practices for financial management. With persistence and the right strategies, you can overcome destructive financial patterns and achieve long-term financial success.

FAQ

What are some common financial habits that can ruin my finances?

Common financial habits that can negatively impact your finances include impulse spending, living paycheck to paycheck, mismanaging credit cards, and neglecting financial education and planning.

How can daily financial decisions impact my financial health?

Daily financial decisions, though seemingly insignificant on their own, can collectively have a substantial impact on one’s financial health over time due to the compounding effect of small choices.

What is impulse spending, and how can I resist it?

Impulse spending refers to making unplanned purchases, often triggered by emotional factors or marketing tactics. To resist impulse spending, it’s essential to identify your emotional triggers, be aware of marketing strategies, and implement practical methods such as creating a budget and practicing mindful spending.

How can I break the cycle of living paycheck to paycheck?

To break the cycle of living paycheck to paycheck, you can create more flexibility in your monthly budget by prioritizing needs over wants, reducing expenses, and building an emergency fund to mitigate financial stress.

What is the impact of social media on my spending habits?

Social media can pressure individuals into overspending to “keep up” with others, contributing to financial strain. Being aware of this influence and making conscious spending decisions can help mitigate its impact.

How can subscription services drain my budget?

Subscription services can quietly drain your budget through the cumulative effect of small monthly fees, forgotten subscriptions, and automatic renewals. Regularly auditing and optimizing your digital expenses can help prevent unnecessary financial leakage.

What are the dangers of credit card mismanagement?

Credit card mismanagement can lead to debt accumulation due to making only minimum payments and the impact of interest rates. Strategic approaches to paying off credit card debt, such as paying more than the minimum and consolidating debt, can help mitigate this issue.

Why is financial education important?

Financial education is crucial in preventing financial illiteracy, which can have significant costs. Building your financial knowledge base through resources such as books, online courses, and financial advisors can empower you to make informed financial decisions.

How can I start planning for retirement?

Starting retirement planning involves understanding the mathematics of delayed retirement savings and taking simple steps to begin investing, regardless of age. Prioritizing retirement planning during your prime working years can significantly impact your financial security in the long run.

What are some strategies for breaking destructive financial patterns?

Breaking destructive financial patterns involves recognizing and changing detrimental financial habits, adopting healthier financial behaviors, and implementing positive change through education, planning, and discipline.

If you liked this article please give it some claps before going and follow me because I will bring more content like this in future

And, to have stories sent directly to you, subscribe to my newsletter.